2024-06-10, Xin Guo (UC Berkeley), TBD

2024-05-30, Paolo Guasoni (Dublin City University), TBD

2024-05-23, Huyên Pham (Université Paris Cité), TBD

2024-04-23 to 04-26, Workshop at the Beijing International Center for Mathematical Research (BICMR)

2024-04-11, Vincent Bogousslavsky (Boston College), A Century of Market Reversals: Resurrecting Volatility

2024-03-28, Ciamac Moallemi (Columbi University), The Economics of Automated Market Making and Decentralized Exchanges

2024-03-14, Mehmet Saglam (University of Cincinnati), Optimal Dynamic Asset Allocation with Transaction Costs: The Role of Hedging Demands

2024-03-07, Roger Lee (University of Chicago), All AMMs are CFMMs. All DeFi markets have invariants. A DeFi market is arbitrage-free if and only if it has an increasing invariant

2024-02-29, Alberto Martín-Utrera (Iowa State University), Do Limits to Arbitrage Explain Portfolio Gains from Asset Mispricing?

2023-12-14, Kiseop Lee (Purdue University), Attention-Based Reading, Highlighting, and Forecasting of the Limit Order Book

2023-12-14, Thomas Ernst (University of Maryland), Would Order By Order Auctions Be Competitive?

2023-11-30, Yuanying Guan (DePaul University), Ambiguity Aversion and State-of-Information-Dependent Insurance

2023-11-17, Paul Glasserman (Columbia University), School Colloquium, Does Overnight News Explain Overnight Returns?

2023-11-09, Luitgard A. M. Veraart (London School of Economics and Political Science), Systemic Risk in Markets with Multiple Central Counterparties

2023-11-07, Ruodu Wang (University of Waterloo), A theory of credit rating criteria

2023-11-07, Fangda Liu (University of Waterloo), Distributional uncertainty with loss functions

2023-10-26, Ning Cai (Hong Kong University of Science and Technology (Guangzhou)), Data Collection and Machine Learning with Privacy Preservation

2023-10-12, Lan Zhang (University of Illinois at Chicago), Nonparametric Standard Errors for High Frequency Data: The Continuous Time Observed Asymptotic Variance (C-AVAR)

2023-09-28, Ioanid Rosu (HEC Paris), Multi-Asset Market Making

2023-06-15, X. Sheldon Lin (University of Toronto), Insurance Risk Classification via a Mixture of Experts Model with Random Effects

2023-06-14, Mao Ye (Cornell University), Bridging the Gap Between Financial Engineering and Finance Communities: Opportunities and Challenges Led by the Big Data

2023-06-01, Peter Tankov (ENSAE, Institute Polytechnique de Paris), Decarbonization of large financial markets

2023-05-25, Dacheng Xiu (University of Chicago), The Statistical Limit of Arbitrage

2023-05-11, Xi Yuan (China Reinsurance), The Climate related financial risks and risk analysis methods

2023-04-06, Jean-Edouard Colliard (HEC Paris), Algorithmic Pricing and Liquidity in Securities Markets

2023-03-23, Bart Zhou Yueshen (INSEAD), Less is More

2023-03-09, Alex Chinco (Zicklin School of Business, CUNY Baruch), Proving You Can Pick Stocks Without Revealing How

2023-03-02, Xin Guo (UC Berkeley), Generative Adversarial Networks (GANs): Some Analytical Perspective

2022-12-08, Hao Xing (Boston University), The Cash-Cap Model: a Two-State Model of Firm Dynamics

2022-12-01, Kay Giesecke (Stanford University), Deep Learning for Mortgage-Backed Securities Markets

2022-11-17, Markus Pelger (Stanford University), Deep Learning Statistical Arbitrage

2022-10-27, Zongxia Liang (Tsinghua University), Weak equilibriums for time-inconsistent stopping control problems, with applications to investment-withdrawal decision model

2022-10-13, Xuedong He (Chinese University of Hong Kong), Dynamic Mean-Variance Efficient Fractional Kelly Portfolios in a Stochastic Volatility Model

2022-09-29, Xiaoqun Wang (Tsinghua University), High-Dimensional Challenges for Computational Finance

2022-09-15, Zhijun Zhang (Dingnuo Investment), 债券市场概况及债券评级

2022-09-01, Ying Jiao (Université Claude Bernard Lyon 1), Socioeconomic pathways of carbon emission and credit risk

2022-06-09, Thorsten Hens (University of Zurich), Evolutionary Portfolio Theory [Video Recording]

2022-05-25, Steven Kou (Boston University), FinTech Econometrics: Privacy Preservation and the Wisdom of the Crowd [Poster]

2022-05-12, Special Session with Ruimeng Hu (UC Santa Barbara), Wenping Tang (Columbia University), and Renyuan Xu (University of Southern California) [Poster]

2022-04-28, Lin William Cong (Cornell University), Designing Data-Driven AI Models for Financial Math [Poster]

2022-04-21, Nan Chen (Chinese University of Hong Hong), Two Game Theoretic Approaches to Single- and Multi-Agent Reinforcement Learning [Poster]

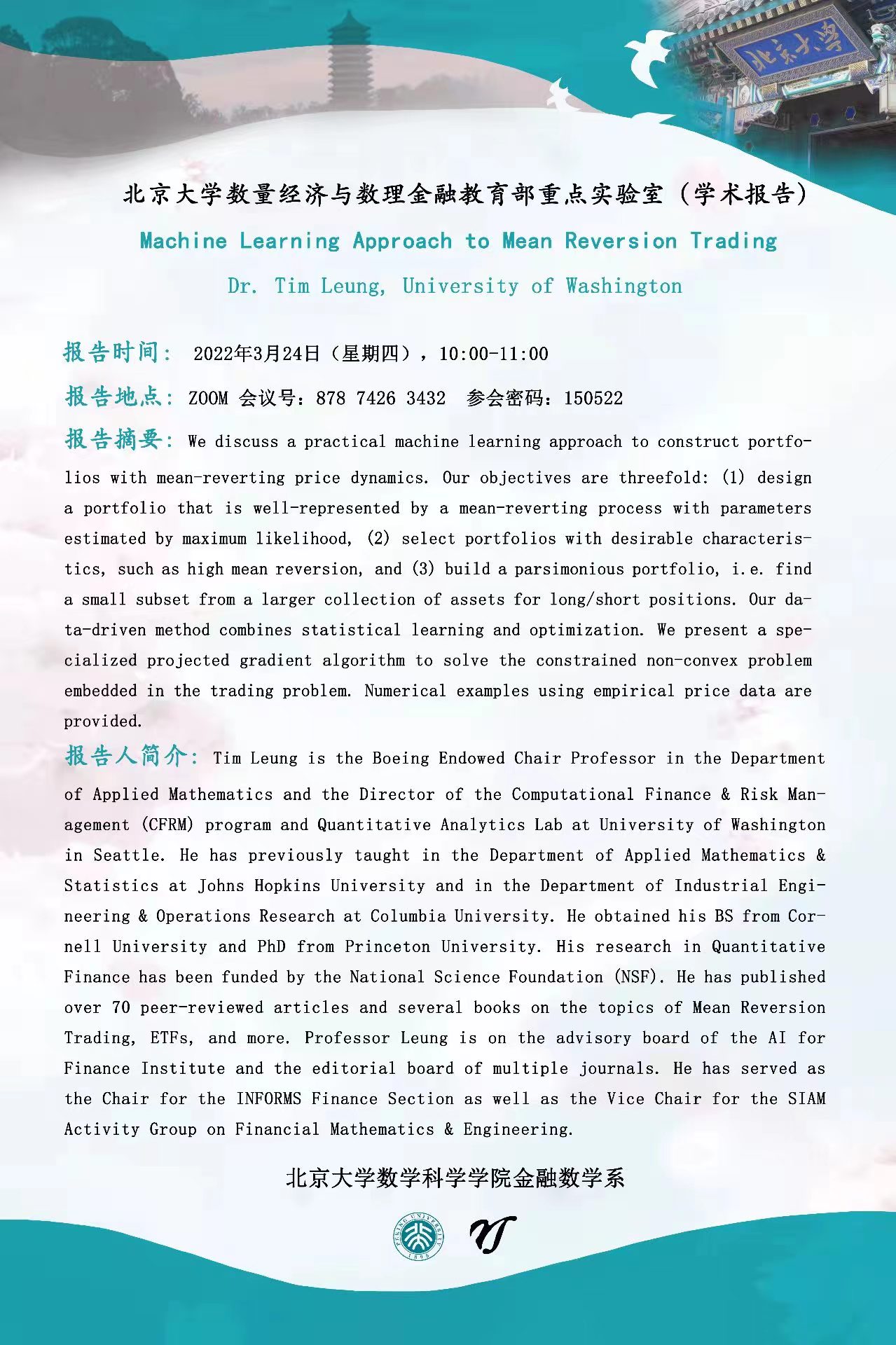

2022-03-24, Tim Leung (University of Washington), Machine Learning Approach to Mean Reversion Trading [Poster]

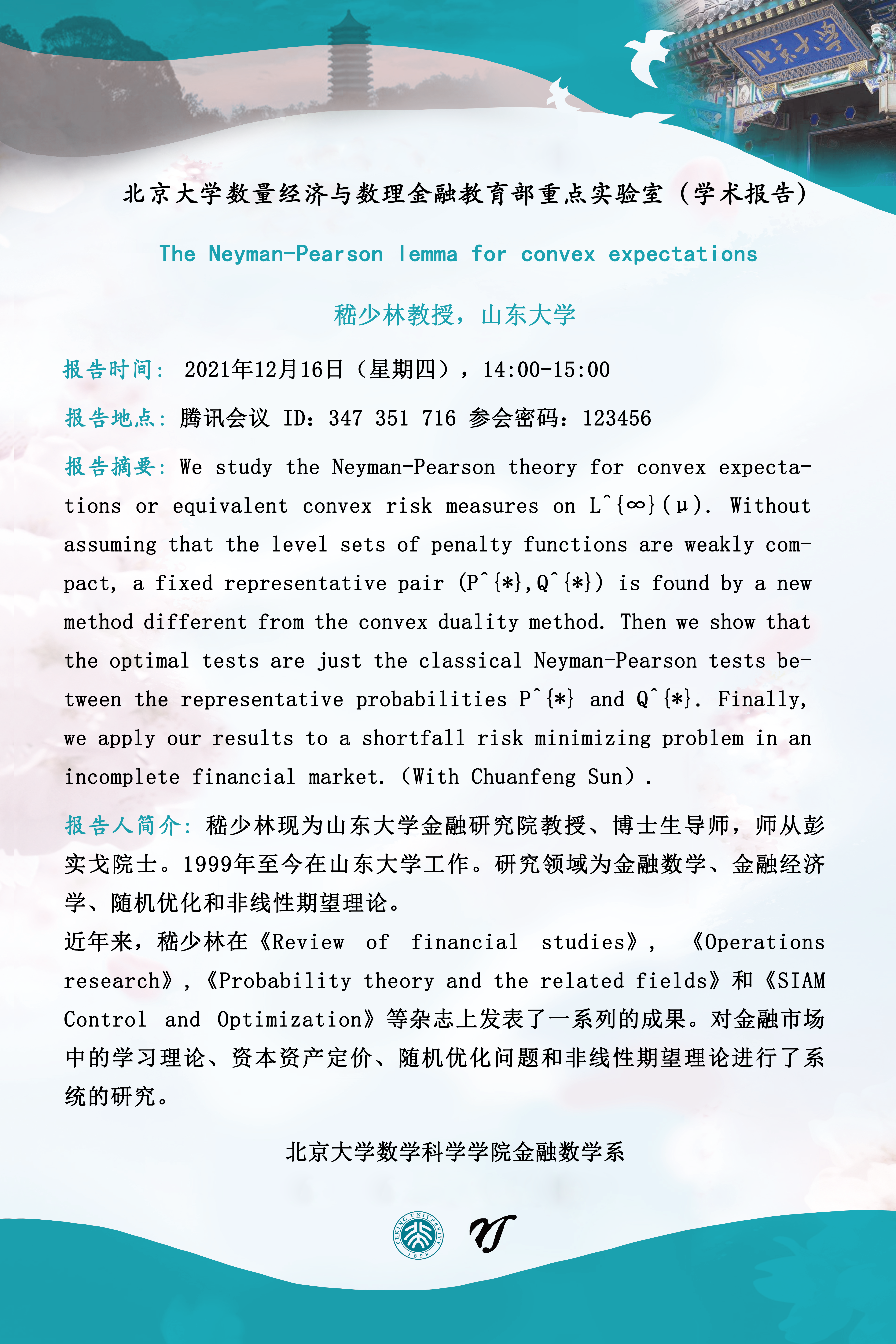

2021-12-16, Shaolin Ji (Shandong University), The Neyman-Pearson lemma for convex expectations [Poster]

2021-12-02, Agostino Capponi (Columbia University), The Adoption of Blockchain Based Decentralized Exchanges [Poster]

2021-11-24, Steve Yang (Steven Institute of Technology), Modeling self-exciting extreme returns in financial market: an AR-GARCH model with Hawkes point processes [Poster]

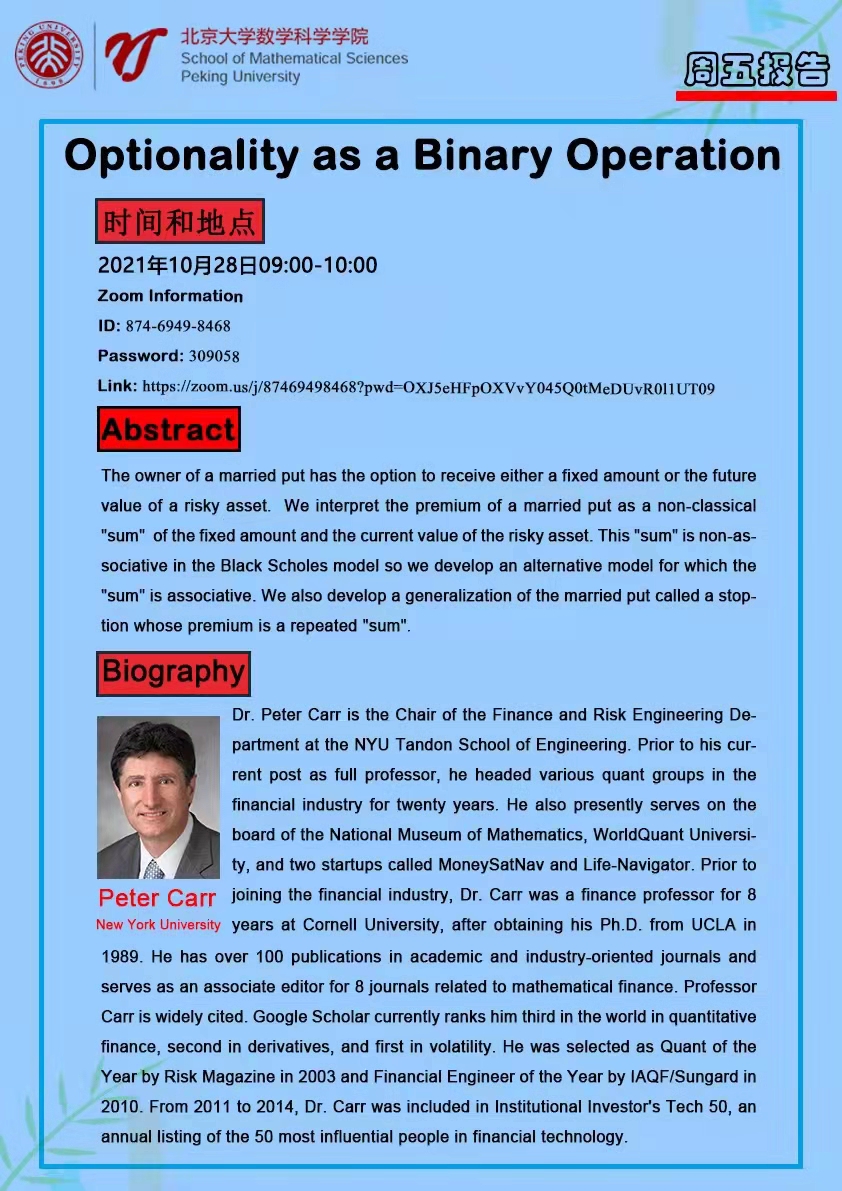

2021-10-28, Peter Carr (New York University), School Colloquium, Optionality as a Binary Operation [Poster] [Video Recording]

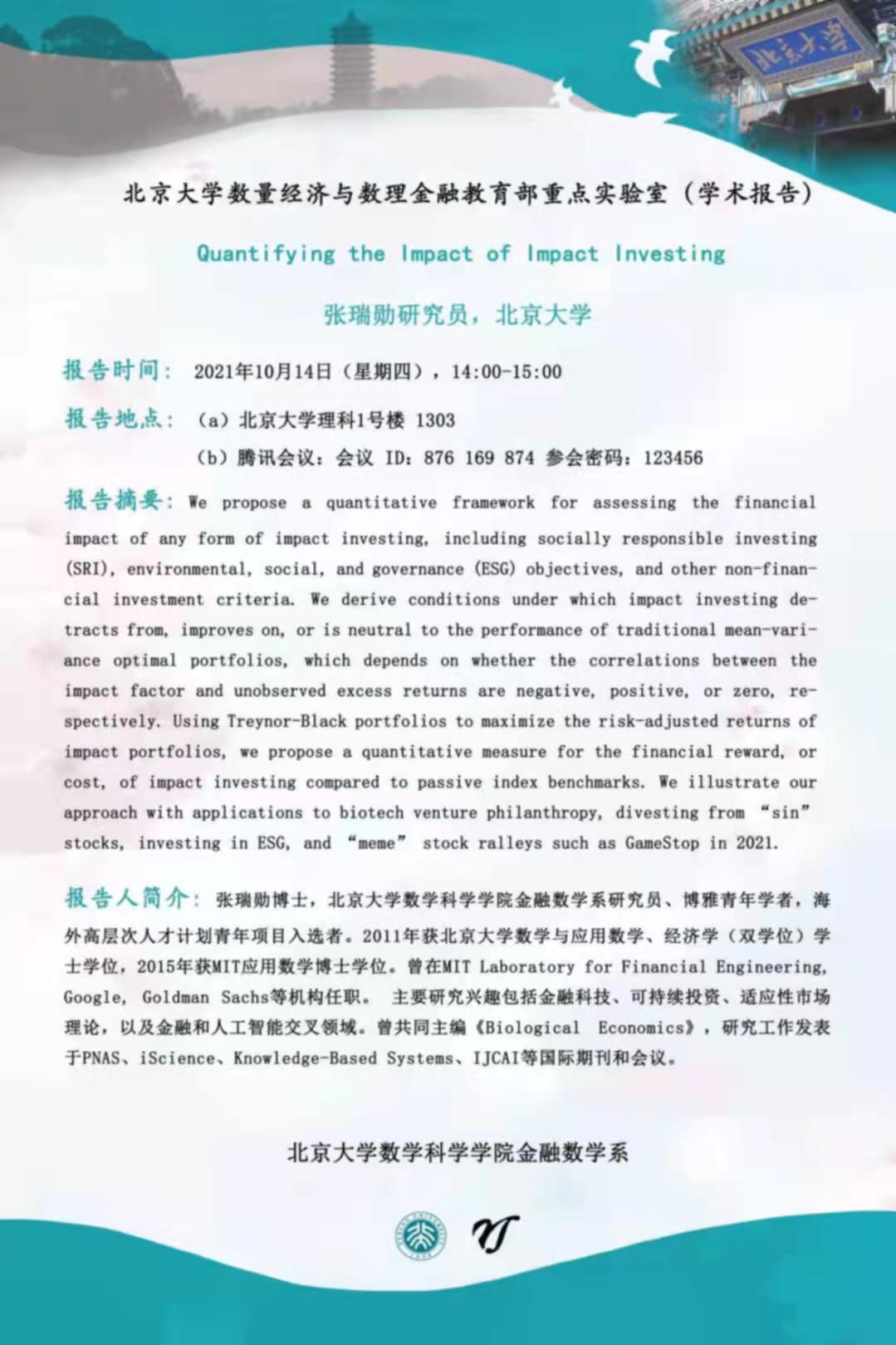

2021-10-14, Ruixun Zhang (Peking University), Quantifying the Impact of Impact Investing [Poster]

2021-09-16, Chen Zhou (Erasmus University Rotterdam), Extreme value statistics in semi-supervised models

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}